Watching the news of Houston breaks my heart; the loss of life, the loss of property, and the total devastation to a city that will take years to recover. The worst storm in our history has almost wiped Houston out completely.

Watching the news of Houston breaks my heart; the loss of life, the loss of property, and the total devastation to a city that will take years to recover. The worst storm in our history has almost wiped Houston out completely.

But for people relying on their insurance to recoup the cost of their home, and maybe repair it, there are harder choices coming.

Many people rely on the National Flood Insurance Program, a program created by Congress in 1968 that enables property owners in participating communities to purchase flood insurance that is administered by the government. It requires flood insurance for all loans or lines of credit that are secured by existing buildings, manufactured homes, or buildings under construction, that are located in a community that participates in the NFIP. This insurance is designed to provide an insurance alternative to disaster assistance to meet the escalating costs of repairing damage to buildings and their contents caused by floods.

Basically, this program was designed to use the government to supplement or even replace flood insurance a person can buy privately. For those in Harvey’s path who have it, it helps to ensure that their homes are insured and can be repaired, or at the very least they can get back the money they sunk into their property should it be beyond repair.

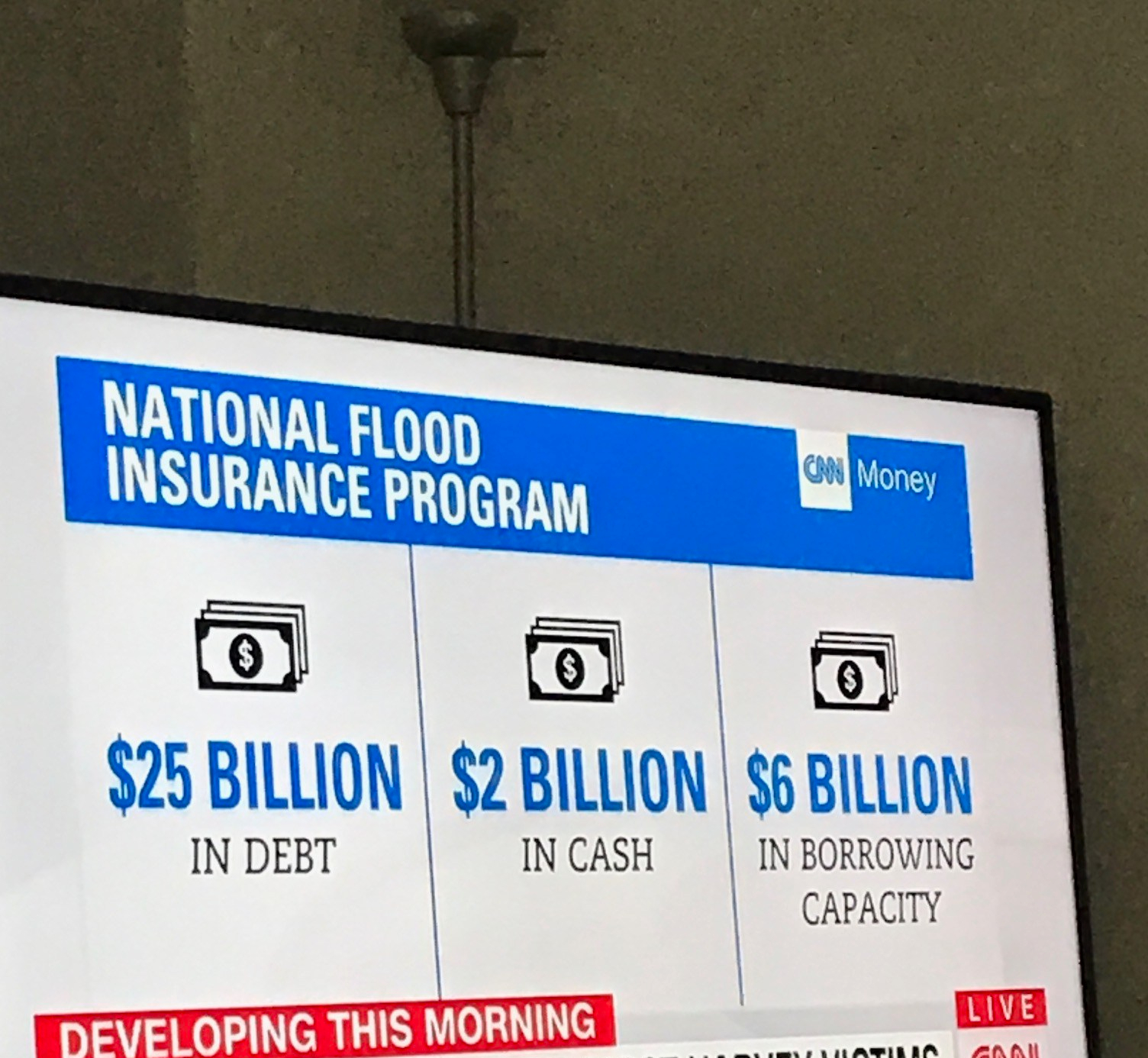

The problem? It’s massively in debt.

As reported by CNN (see graphic at top of the article) the program is twenty-five billion dollars in debt, with two billion dollars in cash on hand for immediate distribution and six billion in borrowing capacity should it need to do so. And with Harvey’s devastation estimated to cost in the double-digit-billions, there is a good possibility that this program could cave, or at the very least be ineffective to address the clean up needs of the city. Every day people are going to struggle to rebuild if this program doesn’t help.

Why the debt? To begin with, Super Storm Sandy affected many homes two years ago and, like Houston, much of the clean up fell under this program. It stressed the program far beyond it’s original intent. Secondly, and this is stressed by scientists near-unanimously, climate change is making storms worse and will continue to do so. They will cause more flooding and damage than previous years. Thirdly, and probably most pressing, that the program is running a 10-to-1 ratio; every 1 percent of houses affected by flooding are causing 10 percent of claims. It’s too much for the system to sustain.

And with the area affected by flooding on the rise (problem 2) and stressing an already indebted program (problem 1) the program could completely collapse. Hopefully, this won’t happen, but if the debt is not addressed and Congress continues to spend, there may not be a way to save it. Unfortunately, it won’t be Congress who runs into a problem. It’ll be every day Americans who were relying on this program, like those in Houston, who will suffer.

Categories: Politics